|

Based on the numbers you supplied, here is your home loan quote. Wish to see other alternatives? Simply go into brand-new numbers to compute and compare. Our company believe that exceptional service and a track record for honesty, integrity and dependability are just as crucial as assisting you discover the house of your dreams. We're experiencing high telephone call volumes and appreciate your perseverance. Numerous questions can be fixed through our automatic response system on-line. If you are requesting COVID-19 payment assistance, please email us at. Mr. Cooper is here to stroll alongside you in your homeownership journey in Brea, CA. As the third-largest home loan servicer and a top-20 house lender in the country, we have the background to help you examine your loan options and solidify your home purchasing plan. A Mr. Cooper home mortgage professional can develop a customized method that will assist you take on the house loan process with confidence. Our mortgage experts will evaluate your unique monetary and living circumstance and will develop a recommended strategy for the best mortgage alternatives that fit your needs. Discover more about numerous house mortgages below and contact Mr. Cooper in Brea to take the initial step toward reaching your objective. The Greatest Guide To What States Do I Need To Be Licensed In To Sell Mortgages

About 1 in 5 of all property buyers go with this kind of government-insured loan. The loan system is specifically geared toward homebuyers who can't pay for the common 20% down payment that's typically required by personal lending institutions. The down payment can be as low as 3. 5% and may be a perfect suitable for buyers who can't get a conventional loan. Cooper has enjoyed FHA loans increase in popularity alongside increases in trainee loan debt and rental costs two situations that can make it difficult to put away cash for a deposit. Another perk to FHA loans is that they're typically readily available to debtors with lower credit history. Wherever you are on your journey, Mr. There's no concern about it. America's service members, veterans, and their spouses must receive the best. Mr. Cooper can lend their knowledge in assisting you get More help received a VA mortgage in Brea if you think you might be qualified for one. Get In Touch With Mr. mortgages what will that house cost. Cooper if you're looking to buy a house in Brea and want to discover more about VA loans. VA loans offer lower rates when compared to the general mortgage landscape. There's also a possibility that you won't need to put down a down payment. Confirming your VA eligibility for a VA loan in Brea is quick and basic with a Mr. Cooper expert walking you through the application procedure. A jumbo home mortgage, or a jumbo loan, goes beyond the limitations of a standard loan. Jumbo loans are created to assist people refinance or buy higher-valued realty and are often millions of dollars. If you want to utilize a jumbo loan to purchase a house in Brea, you will most likely require a larger loan amount that goes beyond standard loan limits. The Buzz on How Many Lendors To Seek Mortgages From

Cooper for additional information on jumbo loan eligibility in Brea. Mr. Cooper's team of home loan specialists is ready to assist you through your home purchasing journey in Brea (what is the concept of nvp and how does it apply to mortgages and loans). But we know that does not indicate the exact same thing to everyone. Some individuals simply desire to examine home mortgage rates in Brea. Others wish to get preapproved for a home mortgage in Brea. Sort by: importance - date Page 1 of 2,047 jobs Shown here are Task Advertisements that match your query. Undoubtedly might be compensated by these companies, helping keep Indeed totally free for jobseekers. Certainly ranks Job Ads based upon a mix of company bids and significance, such as your search terms and other activity on Undoubtedly.

Can package loan documents efficiently for financing. From $20,000 a month You will take the NMLS test and start getting accredited in the states Proven Home loan works and start developing your pipeline. Santa Ana, CA 92705 Briefly remote $18 - $32 an hour Quickly applyUrgently employing Verify and examine loan documentation consisting of earnings, credit, appraisal, and title, while preserving strict compliance with all suitable federal and state From $250,000 a year Contact pre-qualified borrowers to facilitate a warm call transfer to a certified Home loan Loan Originator/Banker. From $16 an hour Moreover, this position provides a basic rate wage with the eligibility of commission for each successfully moneyed loan! Costa Mesa, CA 92626 Remote Run MERS for scams audit. Helping funders with jobs as needed. High School diploma or equivalent. 1= years' home mortgage experience in a similar role. Proven experience dealing with CRM software application. True Home Loan Irvine, CA 92618 Momentarily remote $120,000 - $500,000 a year Easily applyUrgently employing We supply all of our loan officers direct to consumer marketing with inbound calls, a generous indication on warranty, and a comp strategy varying from 30 -100 basis Quickly applyUrgently hiring A great job for somebody just entering the labor force or going back to the labor force with minimal experience and education. A Biased View of When Did Subprime Mortgages Start In 2005

$ 15 - $18 an hour Easily applyUrgently employing _ We will train the very best of the very best in this department to end up being certified Loan Officers. Multi-task effectively by speaking and getting in client data. Delegate Financing Irvine, CA 92602 (Lower Peters Canyon area) From $14 an hour Become a certified home mortgage lender in less than 6 months. $ 55,000 - $60,000 a year Easily applyUrgently hiring Acquainted with regulative requirements concerning disclosures and home loan files. Carry out file evaluations while adhering to regulatory compliance and time Work with Department Manager and Loan Officers on local marketing projects utilizing Mortgage Returns, Eaglehm. com leads, etc. Communicate well with co-workers. Monday Friday 9 a. m. 5 p. m. Saturday 9 a. m.-1 p. m. 2500 E. Imperial Hwy. Suite 170Brea, CA 92821 Serving CU SoCal Members more info and CO-OP shared branch Members in Brea on the corner of Imperial Highway and Kraemer Boulevard. For check and cash deposits, and cash withdrawals, there is likewise a CU SoCal ATM available with 24-hour gain access to. Holiday Date Observed New Year's Day Friday, January 1 Martin Luther King Day Monday, January 18 President's Day Monday, February 17 Memorial Day Monday, May 25 Independence Day Friday, July 3, and Saturday, July 4 Labor Day Monday, September 7 Veteran's Day (Observed) Wednesday, November 11 Thanksgiving Thursday, November 26 Thanksgiving (Continued) Friday, November 27 Christmas Eve (open until 1 p. Fixed rate home loans are mortgages where the interest rate stays the exact same for the entire term of the loan. The advantage to a fixed rate home mortgage is that if you lock a relatively low rate, your payment will not go up when rates do. With an adjustable rate home loan, the rate of the loan can alter throughout the regard to the loan. The Only Guide to How Reverse Mortgages Work In Maryland

A hybrid loan combines a fixed duration in addition to an adjustable component. Usually these loans are repaired for an amount of time and after that the loan ends up being adjustable where it is reliant on existing rates. An FHA loan is a loan in the United States that is guaranteed by the Federal Housing Administration. The loan might be issued by certified loan Visit this link providers. The VA was developed to use long-term funding to American Veterans or to their enduring partners.

0 Comments

It is not to your advantage to delay notifying your servicer [deadlines tend to be] based upon the date that the customer died not the Find more information date that the loan servicer was warned of the customer's death." Do not be alarmed if you receive a Due and Payable notification after alerting the loan servicer of the customer's death. The loan servicer will provide you as much as 6 months to either settle the reverse mortgage financial obligation, by selling the residential or commercial property or using other funds, or buy the home for 95% of its current evaluated value. You can ask for as much as two 90-day extensions if you require more time, but you will have to demonstrate that you are actively working toward a resolution and HUD will have to approve your request. Whether you want to keep the home, sell it to pay off the reverse home mortgage balance, or ignore the property and let the lending institution handle the sale, it's important to keep in contact with the loan servicer. If, like Everson, you have trouble handling the loan provider, you can submit a grievance https://www.tastefulspace.com/blog/2020/01/08/7-key-things-to-know-before-you-buy-a-timeshare/ with the Consumer Financial Security Bureau online or by calling (855) 411-CFPB. " When the last homeowner dies, HUD begins proceedings to take back the home. This results in a lot more foreclosure proceedings than real foreclosures," he said. If you are dealing with reverse home loan foreclosure, deal with your loan servicer to resolve the situation. The servicer can connect you to a reverse home mortgage foreclosure prevention counselor, who can work with you to set up a payment plan. We get contact a regular basis from individuals who believed they were totally safe in their Reverse Mortgage (likewise called a "House Equity Conversion Home Mortgage") however have now found out they are being foreclosed on. How is this possible if the business who owns the Reverse Mortgage has made this arrangement with the property owner so they can live out their days in the house? The easy response is to look to your contract. 202 defines a House Equity Conversion Home Mortgage as "a reverse mortgage loan made to an elderly house owner, which home loan is secured by a lien on genuine residential or commercial property." It likewise defines an "senior property owner" as someone who is 70 years of age or older. If the home is collectively owned, then both house owners are deemed to be "senior" if a minimum of one of the house owners is 70 years of age or older. Rumored Buzz on How Many Mortgages Can You Take Out On One Property

If these provisions are not followed to the letter, then the home mortgage business will foreclose on the property and you may be responsible for certain costs. Some of these might include, however are not restricted to, default on paying Property Taxes or House owner's Insurance, Death of the Debtor, or Failure to make timely Repairs of the Property. Often it is the Reverse Home loan lending institution that is supposed to make the Real estate tax or pay the Homeowner's Insurance much like a standard home loan might have these taken into escrow to be paid by the lending institution. Nevertheless, it is extremely typical that the Reverse Home mortgage property owner should pay these. The lending institution will do this to safeguard its financial investment in the home. If this is the case, then the most common service is to make certain these payments are made, give the receipt of these payments to the loan provider and you will most likely need to pay their lawyer's costs. Numerous Reverse Home mortgage stipulations will specify that they deserve to accelerate the debt if a debtor passes away and the home is not the primary residence of a minimum of one making it through customer. In the case of Nationstar Mortgage Business v. Levine from Florida's 4th District Court of Appeal in 2017 the owner and his spouse both lived in the residential or commercial property, but Mr. His spouse was not on the home https://www.dreamlandsdesign.com/how-do-timeshares-work-exactly-guide/ mortgage and because Mr. Levine passed away, Nationstar exercised its right to accelerate the debt and ultimately foreclosed. One of the important things that can be performed in this case is for the partner or another relative to purchase out the reverse home loan for 95% of the evaluated value of the residential or commercial property or the actual cost of the financial obligation (whichever is less). The family can buy out the loan if they wish to keep the residential or commercial property in the household. Another circumstances would be that if the property is damaged by some sort of natural catastrophe or from something else like a pipeline rupturing behind a wall. A number of these sort of problems can be dealt with rather rapidly by the homeowner's insurance coverage.

Rumored Buzz on Which Australian Banks Lend To Expats For Mortgages

If it is not repaired rapidly, the Reverse Home loan loan provider could foreclose on the home. Just like the payment of the taxes and insurance coverage, the way to handle this scenario is to right away look after the damage. This might mean going to the insurance business to make certain repairs get done, or to pay of pocket to ensure they get done. In all of these circumstances, it is needed to have a first-class foreclosure defense group representing you throughout of your case. You don't need to go this alone. If you or a relative is being foreclosed on from your Reverse Home mortgage, please offer the Haynes Law Group, P.A. We manage foreclosure defense cases all over the state of Florida and will be able to offer you guidance on what to do while representing you or your member of the family on the Reverse Home mortgage Foreclosure case. what are cpm payments with regards to fixed mortgages rates. The assessment is constantly free. A reverse home mortgage is a type of home loan that is typically offered to homeowners 60 years of age or older that permits you to convert some of the equity in your house into money while you maintain ownership. This can be an appealing alternative for seniors who might find themselves "home rich" but "cash bad," but it is not right for everyone. In a reverse home mortgage, you are borrowing cash versus the amount of equity in your house. Equity is the distinction between the evaluated value of your house and your outstanding home loan balance. The equity in your house rises as the size of your home mortgage shrinks and/or your property worth grows. This means that you are paying interest on both the principal and the interest which has currently accumulated monthly. Intensified interest triggers the impressive quantity of your loan to grow at an increasingly faster rate - what are the interest rates on 30 year mortgages today. This implies that a large part of the equity in your house will be used to pay the interest on the amount that the loan provider pays to you the longer your loan is outstanding. If there is no equity in the home, then I would presume she would allow them to take the home if you or any other beneficiaries do not desire to keep the home at a benefit of. They would set up to take the home either by Deed in Lieu or through foreclosure however Deed in Lieu is far better for the loan provider too. We have seen customers who borrowed more in 2005 2007 than their houses are still worth today. That does not make the loan a bad loan those borrowers got more cash than their house is presently worth and were allowed to live in their homes for 7 9 years without needing to make a single payment and now that the loan is higher than the existing value of the house, they are not needed to pay one cent over the current value towards the benefit of the loan. Numerous of them paid interest on loans that were well above the current worth of the houses when the values dropped and some paid till they might not pay any longer and after that they had no house to reside in any longer and no cash to start over. Your mommy was guaranteed a house to live in for as long as she wanted/could and didn't have to pay any monthly payments for the whole time she lived there (simply her taxes and insurance) (percentage of applicants who are denied mortgages by income level and race). Your mommy has actually made no payments on her loan for the last 9 years. Please forgive me; I am not insensitive to your mama's circumstance (on average how much money do people borrow with mortgages ?). It simply was not the reverse home loan's fault that the entire economy fell apart which home worths plunged. I guess I just look at it a different method, thank goodness mom had a reverse home loan and not a forward home loan that may have needed her to lose the house previously without the defenses that she has actually had. She can vacate at her leisure (another benefit of the reverse home loan) You can find out more and then as soon as she is out and you have actually moved all of her valuables if none of the other member of the family want the home, just call the servicer and tell them she is out. They will transfer to take the residential or commercial property back and you won't even need the assistance of a lawyer. how many mortgages to apply for.

The Best Guide To How Many New Mortgages Can I Open

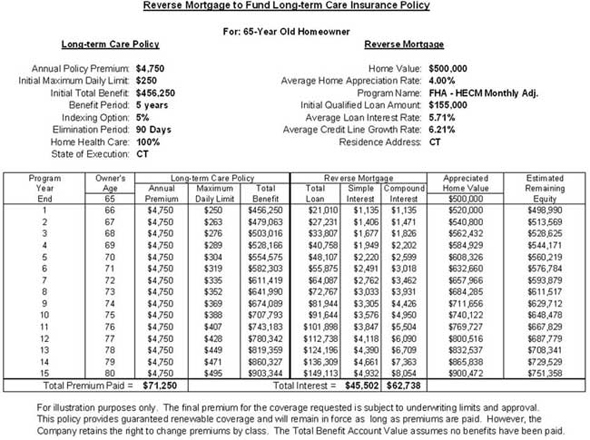

A "non-borrower" is an individual who resides in the home however whose name is not on the loan documents. Typically, the non-borrower need to move when the debtor passes away unless HUD standards qualify them to stay. A "co-borrower" is a person whose name is on the loan files in addition to the property owner (candidate). The sharp recession in the realty market has impacted millions of Americans, and seniors are one of the groups most affected. This is particularly true of senior citizens who have so-called "reverse home mortgages." This type of mortgage can possibly be a great method for individuals over the age of 62 to get money out of their houses. Reverse home loans are not brand-new. However older property owners are progressively relying on them to enhance their circumstances later on in life, specifically during a down economy. These types of mortgages, likewise called Home Equity Conversion Mortgages (HECMs), permit individuals to withdraw some of their home's equity and get it as a swelling sum, in regular monthly payments, as a line of credit or a mix of these options. Property owners qualified for reverse mortgages should be at least 62 years of ages and need to own the home or have a very little exceptional mortgage. The home must be their principal house and house owners should be totally free of any defaults on federal financial obligations. House owners should likewise go to an informational session about reverse mortgages before submitting any HECM loan applications. Due to the fact that of a rash of lending institution foreclosures on primarily elderly property owners holding reverse home loans, the AARP Structure sued the Department of Real Estate and Urban Advancement (HUD), challenging a rule that had the impact of contributing to foreclosures. The rule needed a beneficiary to pay the complete mortgage balance to remain in the house after the borrower's death, even if https://rauter0cmf.doodlekit.com/blog/entry/16782510/some-known-questions-about-how-does-two-mortgages-work the amount was more than the market value of the residential or commercial property.

About How To Reverse Mortgages Work If Your House Burns

Reverse home loans can be expensive and complicated for elderly property owners, as they stand out from standard home loans. Also, a reverse home loan can sometimes deplete all of the equity in the houses if the house owners extend the reverse home mortgage over too long of a period. This typically emerges where the homeowner takes a reverse home mortgage on an assumption of life expectancy, however makes it through well past the anticipated mortality date. This has been specifically true for newly widowed homeowners, and some beneficiaries of debtors, since of lender compliance with an odd HUD rule that was set up in 2008. Prior to the guideline change in 2008, HUD had followed a policy that customers and their heirs would not owe more than a house's value at the time of payment. The 2008 rule mentioned that surviving partners, in order to keep their homes, needed to pay off the reverse mortgage balance shortly after the deaths of their spouses. This held true no matter whether the making it through partner's name was on the loan, and no matter the home's then-current value. That circumstance, and the associated HUD rule, is what prompted AARP to sue HUD. AARP officially challenged HUD's action in altering this guideline, arguing that it was done arbitrarily by letter, rather than through the required administrative treatment. The match further alleged that HUD's guideline change violated protections previously enabled widowed partners to avoid foreclosure. AARP hoped this would prevent additional unlawful foreclosures from reverse home mortgages due at the time of a debtor's death. In April 2011, HUD rescinded the 2008 rule that needed enduring spouses not named on the residential or commercial property's title to pay the complete loan quantity to keep their houses. The ramifications of this change are not yet fully clear. The Best Guide To Mortgages What Will That House Cost

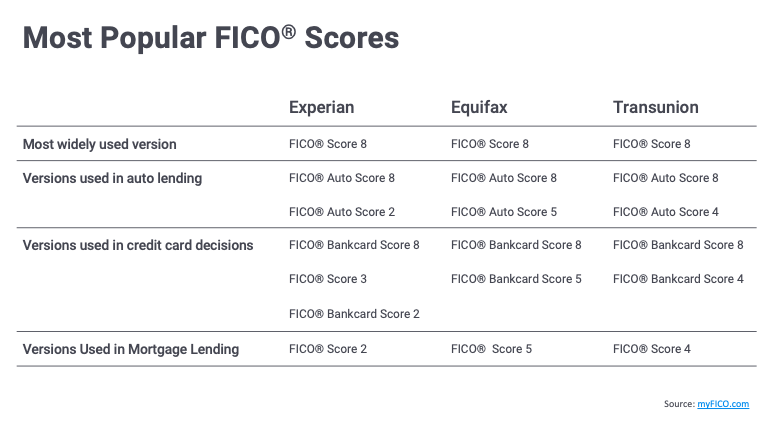

However it is crucial to talk with a skilled realty lawyer to know where you stand. Reverse mortgages ought to provide older house owners more monetary freedom, however when they fail this purpose, they can sadly leave senior people both homeless and powerless. Elderly Twin Cities house owners thinking about participating in a reverse home mortgage contract should seek advice from experienced Minnesota property attorneys like Burns & Hansen, P.A. find out how many mortgages are on a property. In addition, if you currently have a reverse home mortgage on your home, you must discuss your circumstance with a lawyer experienced in these types of home loans to make certain you and your partner are secured if one you dies or if your house loses equity because of the decline of the genuine estate market. A reverse is timeshare worth it mortgage is a method for homeowners ages 62 and older to take advantage of the equity in their home. With a reverse home mortgage, a property owner who owns their house outright or at least has substantial equity to draw from can withdraw a part of their equity without having to repay it up until they leave the house. Credit rating usually range in between 300 to 850 on the FICO scale, from poor to outstanding, calculated by 3 significant credit bureaus (TransUnion, Experian and Equifax). Keeping your credit complimentary and clear of financial obligation and taking the actions to enhance your credit history can qualify you for the finest mortgage rates, repaired or adjustable. They both share similarities in that being effectively prequalified and preapproved gets your foot in the door of that brand-new house, however there are some distinctions. Offering some basic monetary information to a property representative as you go shopping around for a home, like your credit history, present earnings, any financial obligation you may have, and the amount of cost savings you might have can prequalify you for a loan-- generally a way of allocating you in advance for a low-rate loan before you have actually requested it. When you're purchasing a loan, bear in mind: Lower preliminary rate which might be locked for an initial period or set timeframe Rate changes on pre-determined dates (e. g., yearly, 3-, 5-, 7-year terms) Good option if rates of interest are high and/or if you just prepare to remain in the home for a short time Rate of interest stays the very same over the life of the loan Foreseeable monthly paymentseven if rate of interest rise, your payment does not change Great option if interest rates are low and/or you plan to remain in the house for a very long time In some cases these terms are used interchangeably, however they're actually extremely different: This involves providing your lender with some basic informationwhat income you make, what you owe, what properties you have, and so on. When you get pre-qualified, the lending institution doesn't evaluate your credit report or make any decision if you can qualify for a mortgagethey'll just offer the home loan quantity for which you may qualify. Pre-qualifying can help you have a concept of your funding quantity (and the process is normally quick and free), but you won't understand if you actually qualify for a home loan up until you get pre-approved. how do down payments work on mortgages. You'll normally need to pay an application fee, and the loan provider pulls and examines your credit. A pre-approval takes longer than a pre-qualification as it's a more extensive review of your finances and credit value. Pre-approval is a bigger step however a better commitment from the lender. If you get approved for a home mortgage, the loan provider will have the ability to provide: the quantity of funding; potential rate of interest (you might even be able to lock-in the rate); and you'll be able to see an estimate of your regular monthly payment (before taxes and insurance coverage due to the fact that you have not discovered a home yet). Likewise, you're letting sellers understand you're a major and qualified buyer. Typically, if there's competition for a home, buyers who have their financing in place are preferred since it reveals the seller you can pay for the home and are all set to acquire. We'll also go through the pre-approval procedure a bit more in the next section. The interest rate is what the lending institution charges you to borrow cash. The APR consists of the rates of interest along with other fees that will be consisted of over the life of the loan (closing costs, fees, etc) and shows your total yearly expense of borrowing. As a result, the APR is greater than the easy interest of the home loan. Some Ideas on Which Bank Is The Best For Mortgages You Should Know

In addition, all lenders, by federal law, have to follow the same guidelines when determining the APR to ensure precision and consistency. One point is equivalent to one percent of the total principal quantity of your home loan. For instance, if your mortgage amount is going to be $125,000, then one point would equal $1,250 (or 1% of the amount funded). Lenders regularly charge points to cover loan closing costsand the points are typically gathered at the loan closing and might be paid by the borrower (homebuyer) or home seller, or may be divided in between the buyer and seller. This might depend on your local and state regulations in addition to requirements by your lending institution. Make sure to ask if your home loan contains a pre-payment penalty. A pre-payment charge suggests you can be charged a charge if you pay off your home mortgage early (i. e., pay off the loan prior to the loan term ends). When you get a home mortgage, your timeshare exit com lender will likely use a standard form called a Uniform Residential Home Loan Application, Type Number 1003. It is essential to provide accurate information on this kind. The form includes your personal info, the purpose of the loan, your earnings and possessions and other info required throughout the certification procedure - what does ltv mean in mortgages. After you provide the lender six pieces of info your name, your earnings, your social security number to acquire a credit report, the property address, a price quote of the value of the residential or commercial property, and the size of the loan you desire your lender must offer or send you a Loan Price quote within 3 days. e., loan type, rate of interest, estimated monthly home mortgage payments) you went over with your lender. Carefully examine the estimate to be sure the terms meet your expectations. If anything appears different, ask your lender to discuss why and to make any essential corrections. Lenders are required to offer you with a written disclosure of all closing conditions 3 service days prior to your set up closing date. e, closing expenses, loan quantity, rate of interest, month-to-month home loan payment, approximated taxes and insurance coverage beyond escrow). If there are substantial modifications, another three-day disclosure duration might be needed. What Is The Current Interest Rate For Mortgages? Fundamentals Explained

Unless you can buy your house entirely in money, finding the best residential or commercial property is only half the fight. The other half is choosing the very best type of home mortgage. You'll likely be repaying your home loan over a long period of time, so it is necessary to find a loan that satisfies your needs and spending plan.

The 2 main parts of a home loan are primary, which is the loan quantity, and the interest charged on that principal. The U.S. government does not work as a home mortgage loan provider, however it does guarantee specific types of home mortgage loans. what happens to my timeshare if i die The six main types of home mortgages are conventional, conforming, non-conforming, Federal Real estate Administration-insured, U.S. Department of Agriculture-insured. There are 2 components to your mortgage paymentprincipal and interest. Principal describes the loan quantity. Interest http://messiahnoct757.cavandoragh.org/the-definitive-guide-to-reddit-how-finances-and-mortgages-work is an additional amount (calculated as a portion of the principal) that lending institutions charge you for the advantage of borrowing money that you can pay back with time. Throughout your home loan term, you pay in regular monthly installations based upon an amortization schedule set by your lender. APR includes the interest rate and other loan fees. Not all mortgage products are created equivalent. Some have more strict standards than others. Some loan providers may need a 20% deposit, while others require as low as 3% of the house's purchase price. To certify for some types of loans, you need beautiful credit. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

/find-and-compare-best-mortgage-rates-4148342_FINAL-d90ea8095a49474f90bee793bf4c5918.png)

RSS Feed

RSS Feed